Introduction

The tax season is not a time to get stressed. By being smart in planning, you can take advantage of tax laws and still comply with the law. Welcome to Tax Planning 101—your ultimate guide for realizing, controlling, and utilizing tax savings. Tax planning is not an option—it is a necessity for everyone, whether you are a salaried employee, a business owner, a freelancer, or an investor.

Table of Contents

What is Tax Planning?

Tax planning is a method of examining financial information and paying an income tax in a manner that minimizes the taxpayer’s tax liability. Tax evasion, illegal as it is, is the direct opposite of legal tax planning under the Income Tax Act.

- Legally reduce your tax liability

- Ensure compliance with tax

- Make the most from the investment

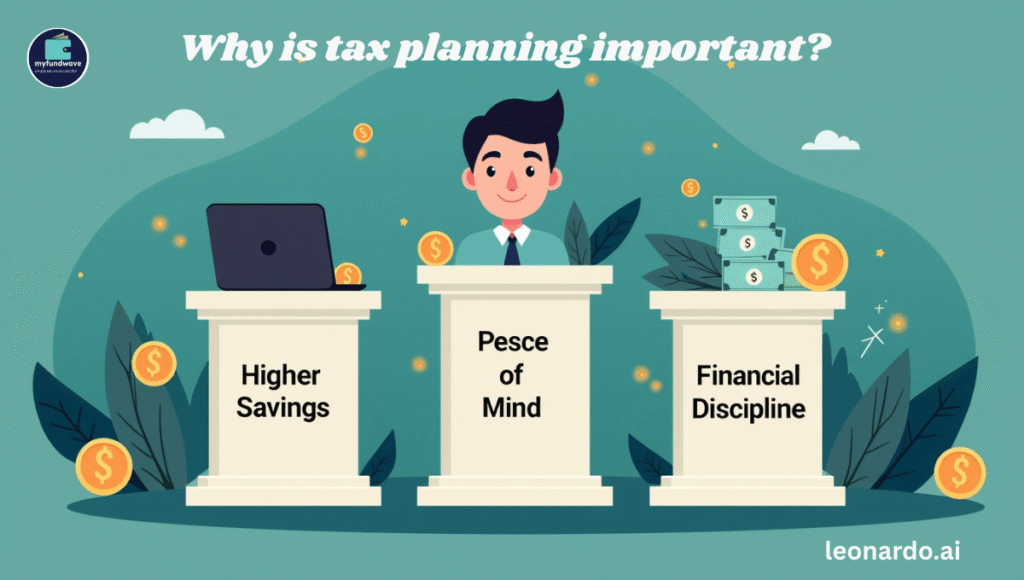

Why is tax planning important?

- Higher savings: there will be more money for other goals

- Peace of mind: there will be no hassle when the time comes for tax filing

- Financial discipline: it’s easier to be an investor

Intelligent Legal Methods of Tax Saving in 2025

1. Utilize Section 80C up to the maximum

The Income Tax Act’s Section 80C empowers the taxpayer to take advantage of deductions of up to 71.5 lakh. Investments that qualify for tax benefits are:

- Public Provident Fund (PPF)

- Employee Provident Fund (EPF)

- ELSS Mutual Funds

- Life Insurance Premiums

- Tax-saving FDs (5 years)

2. Choose the New vs Old Tax Regime Wisely

From FY 2023-24, the new tax regime is default. Based on the deductions, compare both tax regimes. If you declare lots of exemptions (like HRA, 80C), the old regime could save you extra cash.

3. Claim HRA (House Rent Allowance)

For salaried employees who are tenants and have rent expenses, claiming HRA is the best option for reducing your taxable income. Please keep your rent receipts and the PAN of the landlord with you (if the annual rent exceeds ₹1 lakh).

4. Obtain Tax Benefits Through Health Insurance – Section 80D

Amounts paid for health insurance are eligible for deduction up to:

- $25,000 (self/family under 60)

- 750,000 (senior citizens)

5. National Pension Scheme (NPS) Investment

Under Section 80CCD(1B), NPS contributions can give you an additional ₹50,000 exemption—over and above 80C.

6. Leverage Education Loan Interest – Section 80E

In case you are reimbursing for an education loan (for you, your spouse, or your child), the interest paid is totally tax deductible for 8 years straight.

7. Make Use of Home Loan Benefits

- Principal repayment: under 80C (R1.5 lakh)

- Interest under Section 24(b) (R2 lakh)

8. Submit ITR on Time

The act of filing a tax return later will lead to suffering penalties and losing a refund on interest benefits. Thus, always submit before July 31 unless the deadline is extended.

Common Mistakes to Avoid

- Waiting until March for investment

- Not keeping documentation organized

- Selecting an incorrect tax regime

- Failure to take deductions like 80D, 80E, and 80G (donations) into account.

Conclusion

Smart tax planning isn’t about tax evasion, it is about the legitimate economic efficiency of the tax. It only takes a little bit of alertness and punctuality to save a lot of money every year. Start working right away, schedule the tax payment in time and watch your money get you much richer.