Introduction

As of 2025, the secret to investing no longer exists. Yet, almost every newcomer asks a single question:

“Is it better to start small with ₹1,000 SIP or bold with ₹10,000 SIP?”

But, in reality, the solution rests in numbers, time, and discipline.

If you’re attempting to find out ₹1,000 vs ₹10,000 SIP: which grows more by 2030, you’re on the right page. We will analyze how both values perform in the next five years, what return you can expect, and most importantly, which one is better suited to your lifestyle and financial objectives.

In this post, we’ll compare ₹1,000 vs ₹10,000 SIP under realistic return expectations, walk through the math, and reveal the best strategies to grow your wealth—no matter your income level.

Table of Contents

Why SIPs are the Smartest Investment in 2025

A. The Power of Compounding

SIP (Systematic Investment Plan) is a systematic way of investing in mutual funds. Whether you invest ₹1,000 or ₹10,000 every month, you enjoy compounding, meaning your gains also begin earning returns.

The longer you remain invested, the stronger compounding gets. That’s why early investment—even with a small sum—can be significantly beneficial.

B. Rupee Cost Averaging

One of the biggest benefits of SIPs is rupee cost averaging. Rather than attempting to time the market, you invest at fixed intervals. Occasionally you purchase units at a higher price, occasionally lower. In the long run, this works out and minimizes your risk.

This applies to both ₹1,000 and ₹10,000 SIPs. The only variation? How much wealth you accumulate ultimately.

₹1,000 vs ₹10,000 SIP: Real Growth Numbers by 2030

Let’s dissect it with real calculations. We’ll take two scenarios:

- SIP Tenure: 5 years (2025 to 2030)

- Expected Annual Return: 12% (average equity mutual fund returns)

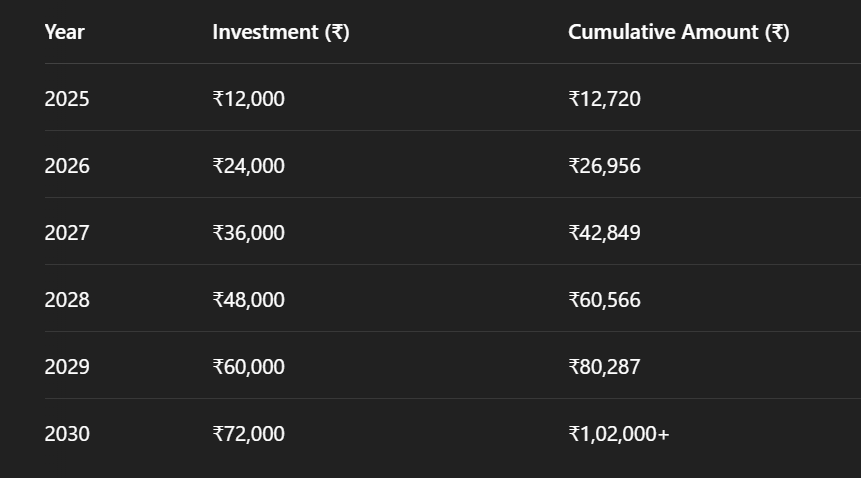

A. ₹1,000 SIP Growth Forecast

By the end of 6 years, a ₹1,000 per month SIP works out to about ₹1.02 lakh.

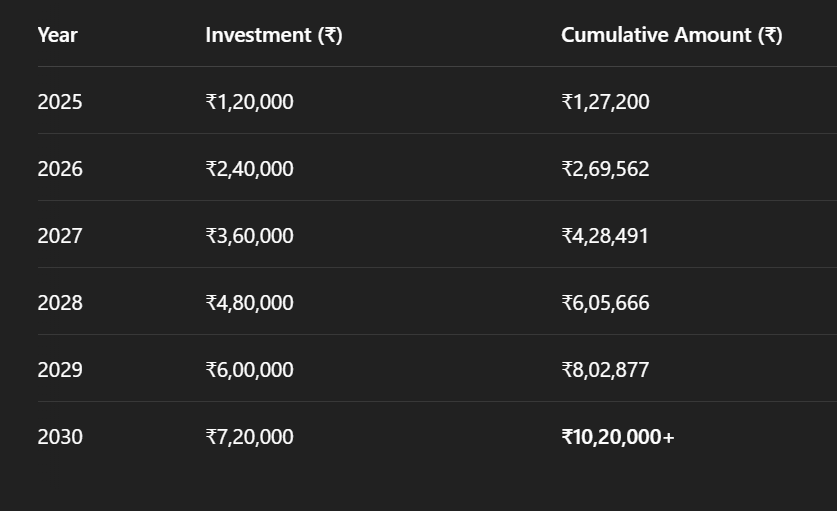

B. ₹10,000 SIP Growth Calculation

Now you can appreciate how the difference is not simply 10x—it becomes so much stronger through compounding.

Result: ₹10,000 SIP accumulates more than ₹10 lakh

₹1,000 SIP crosses ₹1 lakh

The compounding remains the same, but size does count if you are saving for long-term wealth.

₹1,000 vs ₹10,000 SIP: Return Comparison in Different Funds

All money does not yield the same returns. So let’s compare both SIP amounts under various mutual fund categories.

A. Large Cap Mutual Funds (Avg Return ~ 11%)

- ₹1,000 SIP = 797,000 by 2030

- ₹10,000 SIP = 79.7 lakh by 2030

B. Flexi Cap Funds (Avg Return ~ 13%)

- ₹1,000 SIP = 1.07 lakh

- ₹10,000 SIP = F10.7 lakh

C. Small Cap Funds (Avg Return ~ 15%)

- ₹1,000 SIP = 1.15 lakh

- ₹10,000 SIP = {11.5 lakh

C. Small Cap Funds (Avg Return ~ 15%)

- ₹1,000 SIP = 1.15 lakh

- ₹10,000 SIP = {11.5 lakh

“📌 Note: Small-cap funds offer higher returns but also come with higher volatility. Pick based on your risk profile. “

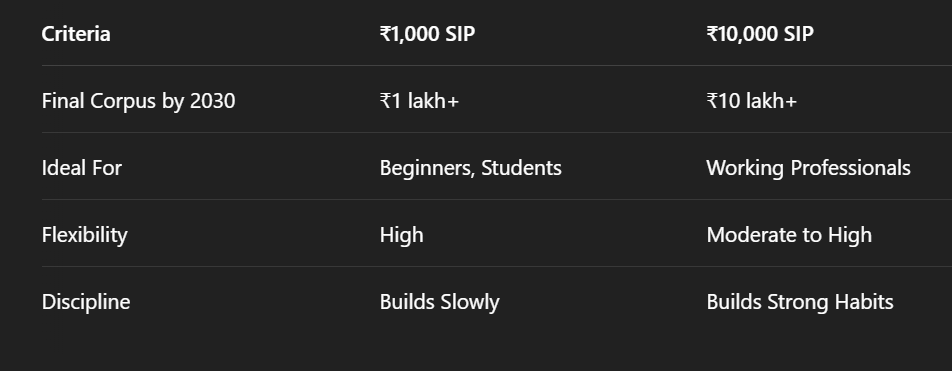

What Kinds of Investor Should Opt for ₹1,000 SIP?

A. Newbies and Low-Income Investors

When you are entering the workforce for the first time or don’t have much spending money, ₹1,000 SIP is ideal. It leads you into investing as a habit, creates persistence, and demonstrates that you can start without breaking the bank.

B. Students or Early Savers

Even college students can initiate SIPs with as little as ₹500–₹1,000 a month through sites such as Groww or Zerodha Coin. Over a period of time, these small investments pave the way for a richer tomorrow.

C. People Testing the Waters

Not ready to commit the whole amount? Beginning with ₹1,000 allows you to watch the market, get familiar with mutual fund websites, and grow your amount as confidence grows.

Who Should Choose ₹10,000 SIP?

A. Mid-to-High Income Earners

If you can manage to spare ₹10,000/month, you’re already set to amass wealth quickly. 5 years of ₹10,000 SIP might be able to reach ₹10 lakh—a fantastic stride toward financial freedom in the long run.

B. FIRE Aspirants

Planning to retire early? ₹10,000 SIP is your best friend. An individual investing ₹10,000 every month for 10 years at 12% can accumulate more than ₹23 lakh, even if he stops putting in money later and leaves compounding to work its magic.

C. Goal-Based Investors

Saving for:

House down payment

- Education of child

- Vacation of a lifetime

Then #10,000 SIP is your best way.

How to Select the Right SIP Amount in 2025

A. Adhere to the 50-30-20 Rule

Apply the rule of investing 20%:

- Salary: €30,000/month → Invest $6,000

- Salary: 50,000/month → Invest *10,000

B. Start Low, Scale Fast

If ₹10,000 seems too much right now, begin with ₹1,000 or ₹2,000 and enable an auto SIP step-up facility. Add ₹500–₹1,000 each year.

C. Utilize Free Tools & SIP Calculators

Utilize sites such as:

- Groww

- Kuvera

- ET Money

To play around with the amounts and observe how your money multiplies.

Avoid Mistakes in SIP Investing

A. Redeeming Too Early

Most investors panic and withdraw during corrections in the market. SIPs are long-term schemes. Keep calm and have faith in the system.

B. Selection Only on Past Returns

Although small-cap funds may appear tantalizing with high returns, they have risk too. Diversify between large, mid, and flexi-cap.

C. Not Considering Tax on Gains

- Equity MFs: LTCG 10% over 71 lakh/year

- Debt MFs: Taxed as per slab (no indexation from 2023)

Plan redemptions wisely to conserve taxes.

Final Verdict: ₹1,000 vs ₹10,000 SIP – Which Wins?

Verdict

- $1,000 SIP: Perfect for habit building. Long-term consistency is better than timing.

- £10,000 SIP: Ideal for serious wealth-building in under 10 years.

But both are preferable to doing nothing. The greatest regret investors have? Not starting

previously.

Conclusion: Begin With What You Have, But Begin Today

Whether you start an SIP for ₹1,000 or ₹10,000, the secret lies in getting going. Your prosperity isn’t in timing the market—it’s about time in the market.

With the ₹1,000 versus ₹10,000 SIP struggle, the real winner is the one who continues steadfastly, goes through highs and lows, and lets the compounding spell work.

So, set up that SIP today. Even if it’s just ₹1,000. Because in five years, you’ll thank yourself for taking that first step.

Nice